Fraud funds are readied to be coated at ₤ 85,000 after regulatory authorities downsized on methods to extend the restriction complying with a response from monetary establishments and political leaders.

The Payment Systems Regulator (PSR) claimed in 2014 that fraud victims dropping nasty of phony “authorised push payments” would definitely be reimbursed by up to £415,000 per claim.

The brand-new rules was due to enter stress from October, but the optimum fraudulence compensation is to be dramatically decreased complying with stable stress from preachers, lending establishments and monetary establishments.

Treasury authorities are comprehended to have really referred to as the ready ₤ 415,000 restriction a “disaster waiting to happen”, main the best way for smaller sized fintech firms to fail.

More than 30 firms apparently approved a letter to the monetary assistant, Bim Afolami, in June requesting the modifications to be stopped briefly.

Consumer groups, nonetheless, have really suggested for the rules to search out proper into impression as a way of providing “vital” protection to fraud victims.

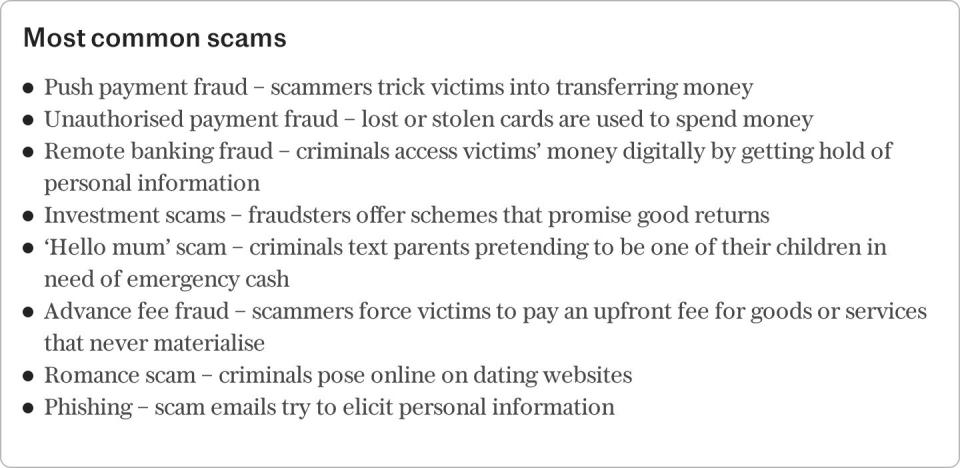

Authorised press repayments (Applications) entail individuals being inspired to voluntarily ship out money from their checking account to the fraudster. The management sometimes focuses on love and acquisition rip-offs, reminiscent of when phony tickets for reveals are marketed.

Last yr alone, deceived customers moved ₤ 460m to fraudsters.

Banks presently compensate customers on a volunteer foundation and are usually not linked proper into obvious guideline.

Monzo and Danske Bank fully reimbursed scammed customers in a lot lower than 10pc of reported software situations, whereas others reminiscent of Nationwide and TSB fully repaid shed funds in larger than 95pc of situations, latest fraud payout figures show.

The PSR actually hoped a compelled optimum fee of ₤ 415,000 would definitely “prevent APP fraud from happening in the first place while ensuring victims are protected in a consistent way”.

Under the brand-new rules, until a goal overlooks cautioning messages from their monetary establishment, falls quick to directly inform their monetary establishment of the fraudulence, rejects to share particulars relating to the fraudulence with the compensation firm or rejects to share data with the cops, they will be entitled to a refund of the money they shed.

The PSR did yield beforehand this yr that the fee technique had “attracted a particularly high level of feedback” and the ready restriction is perhaps modified previous to October.

This outcomes from maintain true in the present day, when the regulatory authority launched a file outlining modifications to the restrict.

An anticipated lower to ₤ 85,000 brings the restriction in accordance with the financial options fee plan (FSCS) which safeguards savers down funds in non-public monetary establishments and growing cultures should they go underneath.

Rocio Concha from the shopper workforce Which? claimed scaling back the payout limit is “outrageous”.

She claimed: “It’s outrageous that the funds regulator is about to water down very important rip-off protections weeks earlier than they have been as a result of take impact and that this transfer follows months of lobbying from corporations that refuse to take fraud critically.

“Slashing the reimbursement limit risks exposing victims of the highest value scams to devastating financial and emotional harm and also significantly reduces crucial financial incentives for payments firms to put in place effective fraud security measures.”

Proposals over the applying compensation restriction come because the regulatory authority prepares handy monetary establishments brand-new powers to freeze payments for up to four days.

Currently, “authorised” repayments– ones which have really been accepted by the shopper– can simply be held for twenty-four hr whereas monetary establishments try.

The regulation, preliminary recommended by the Conservatives and backed by Labour in January, will definitely be pressed with Parliament this fall.

It will definitely present compensation firm an extra 72 hours to take a look at repayments, but simply the place there are wise premises to assume fraudulence or deceit that is perhaps unusual from a shopper’s regular financial activity.