Since the introduction of the net within the mid-Nineteen Nineties, capitalists have truly patiently awaited the next large development forward alongside that may meaningfully change the event trajectory for companyAmerica The arrival of skilled system (AI) is likely to be the response.

Last 12 months, specialists at PwC launched a file (“Sizing the Prize”) that approximated the consolidated consumption-side benefits and efficiency features from AI would definitely embody $15.7 trillion to the globally financial local weather by 2030. If this projection is wherever close to truth, it recommends {that a} plethora of enterprise may find yourself being outstanding victors from the AI change.

Thus a lot, no agency has truly been a bigger recipient of the rise of AI than Nvidia ( NASDAQ: NVDA)— nonetheless this doesn’t suggest Wall Street’s AI beloved has truly made all the best steps.

Nvidia quickly ended up being the enterprise data facility AI gear authority

Pretty lots contemplating that the environment-friendly flag swung, Nvidia’s graphics refining techniques (GPUs) have truly been the favored possibility in AI-accelerated data amenities. Based on value quotes from semiconductor skilled firm TechIn views, 2.67 million GPUs and three.85 million GPUs had been delivered for utilization in enterprise data amenities in 2022 and 2023, particularly. Nvidia represented nearly 30,000 (in 2022) and 90,000 (in 2023) of those GPU deliveries.

Controlling round 98% of {the marketplace} for the GPUs being made use of to take care of generative AI companies and educate huge language designs (LLMs) has truly paid for Nvidia superb charges energy on its game-changing chips. Whereas Advanced Micro Devices is advertising its MI300X AI-GPU for in between $10,000 and $15,000, Nvidia’s H100 GPU briefly coated $40,000 beforehand this 12 months. Overwhelming want, mixed with particular GPU scarcity, has truly led to a melt-up in Nvidia’s modified gross margin.

The agency’s CUDA software program utility system has truly performed an important perform in sustaining organizations trustworthy to its product or companies, as nicely. CUDA is the toolkit that designers make the most of to assemble LLMs and take advantage of the opportunity of their Nvidia GPUs.

Nvidia’s financial second-quarter working outcomes, which data its job from April 29 through July 28, present merely precisely how sturdy want has truly been for its ecological group of companies. Net gross sales expanded by a scorching-hot 122% to cowl $30 billion for the quarter, whereas earnings of $16.6 billion (up 168% year-over-year) as soon as extra blew earlier skilled assumptions.

But not each selection being made by Nvidia’s monitoring group has, maybe, been the best one.

Nvidia’s $50 billion share redeemed consent sends out the inaccurate message to traders

Let me starting this dialog by not concealing that I’ve been a extreme film critic of Nvidia’s appraisal and its historic climb from a $360 billion market cap to a $3 trillion goliath. While figuring out that AI has mass long-lasting attract, I wait my thesis that skilled system is an innovation that requires time to develop. I moreover strongly suppose reasonably priced stress will repeatedly attempt the transcendent GPU charges energy Nvidia has truly appreciated.

But my objection of Nvidia as a monetary funding and agency has a very brand-new emphasis in the present day: the $50 billion share redeemed program licensed by its board, as stored in thoughts within the agency’s second-quarter file. This $50 billion comes atop the $7.5 billion staying from its earlier share buyback program.

Most enterprise license share buybacks for two elements. Firstly, organizations with steady or increasing earnings that redeemed their provide will definitely sometimes see a raise to income per share (EPS). In varied different phrases, earnings is being separated proper right into a smaller sized superior share matter, resulting in better EPS, which may make a agency’s provide additional interesting to principally concentrated capitalists.

The varied different issue a agency’s board accredits share repurchases is to indicate to capitalists that it feels its provide is a deal.

While Nvidia’s $50 billion share redeemed consent is almost definitely targeted on enhancing EPS and instilling self-confidence in its provide, it sends out completely the inaccurate message to Wall Street and traders for 3 elements.

1. Nvidia’s specialists are costing a scorching price

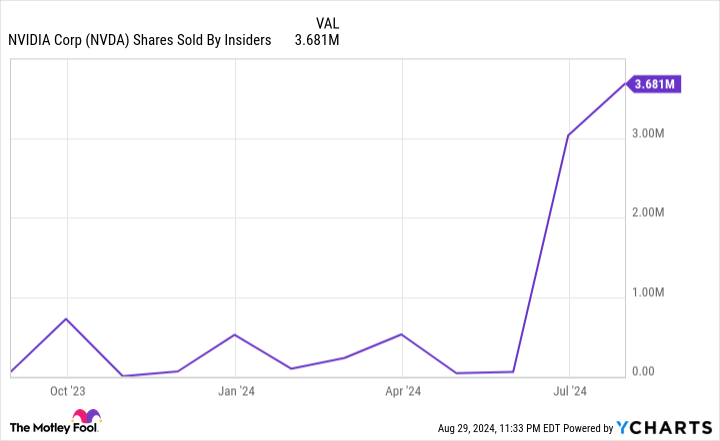

The very first evident drawback with this technique is that skilled advertising job has truly by no means ever been additional noticable. Between mid-June and mid-August, CHIEF EXECUTIVE OFFICER Jensen Huang disposed of 4.8 million shares of his agency’s provide over 20 buying and selling periods, finishing virtually $580 million.

Moreover, the final time an Nvidia skilled acquired a solitary share of their agency’s provide on the aggressive market was December 2020.

The agency’s board merely licensed a large buyback all through a period of unmatched skilled advertising job, which has truly accomplished north of $1.6 billion over the trailing-12-month period. What kind of message does this ship out when specialists won’t buy a solitary share on the aggressive market, nonetheless the board wishes you to suppose the agency’s shares are nonetheless a wonderful value?

2. The agency simply has $34.8 billion in money cash, money cash matchings, and invaluable protections

Another issue this $50 billion share redeemed consent is an epically unfavourable selection by Nvidia is because it completed the financial 2nd quarter with “only” $34.8 billion in money cash, money cash matchings, and invaluable protections in its depository.

To be cheap, Nvidia has truly been a positive capital maker in present quarters, and the agency’s share buyback program has no finish day. Nevertheless, $50 billion is much more of a pie-in-the-sky goal than one thing that’s the truth is potential anytime shortly.

I’ll moreover embody on this issue that $50 billion in share buybacks at Nvidia’s closing price onAug 29 would simply decrease its superior share matter by (drum roll) 1.62%! That’s an incredible deal money to have virtually no affect on EPS.

3. Nvidia cannot find a much better utilization for $50 billion whereas on the main facet of the very best development?

Lastly, it’s just about incomprehensible that Nvidia is focusing on as a lot as $50 billion in additional share repurchases when it’s main the fee (within the meantime) in data-center AI gear.

In order to maintain is calculating profit( s) in AI-accelerated data amenities, Nvidia will definitely require to boldy buy r & d. Although the launch of its next-generation Blackwell GPU type is nearing, and chief govt officer Jensen Huang only recently teased the Rubin system, which will definitely be launched in 2026, you would definitely assume a game-changer like Nvidia may find a much better utilization for $50 billion on the ingenious entrance than merely redeeming its provide to, presumably, improve its quarterly EPS by a few dimes.

With potential restrictions at chip makers reducing Nvidia’s development– Nvidia is fabless and outsources its chip manufacturing– I’d assume a a lot significantly better utilization for $50 billion would definitely be to find means to decrease or take away these provide chain constraints. Acquiring additional potential or construction manufacturing facilities to resolve these issues would definitely make far more feeling than a $50 billion buyback program that effectively signifies that the board and monitoring group haven’t any significantly better ideas.

It’s wanting progressively almost definitely that Nvidia’s splendid days stay within the rearview mirror.

Should you spend $1,000 in Nvidia in the present day?

Before you buy provide in Nvidia, take into account this:

The Motley Fool Stock Advisor skilled group merely decided what they suppose are the 10 splendid provides for capitalists to buy presently … and Nvidia had not been amongst them. The 10 provides that made it’d generate beast returns within the coming years.

Consider when Nvidia made this guidelines on April 15, 2005 … when you spent $1,000 on the time of our referral, you would definitely have $720,542! *

Stock Advisor provides capitalists with an easy-to-follow plan for fulfillment, consisting of recommendation on growing a profile, routine updates from specialists, and a couple of brand-new provide selections each month. The Stock Advisor resolution has better than quadrupled the return of S&P 500 contemplating that 2002 *.

See the ten provides “

*Stock Advisor returns since August 26, 2024

Sean Williams has no placement in any one of many provides mentioned. The Motley Fool has placements in and suggests Advanced Micro Devices andNvidia The Motley Fool has a disclosure plan.

Nvidia’s $50 Billion Share Buyback Is an Epically Bad Decision That Sends the Wrong Message to Wall Street and Investors was initially launched by The Motley Fool